A Brief History Of NFTs: From Invention To Widespread Acceptance

What began in 2012–2013 with coloured coins based on Bitcoin became a phenomenon in 2021 and is still going strong. The widespread adoption of NFTs was greatly aided by the Ethereum blockchain.

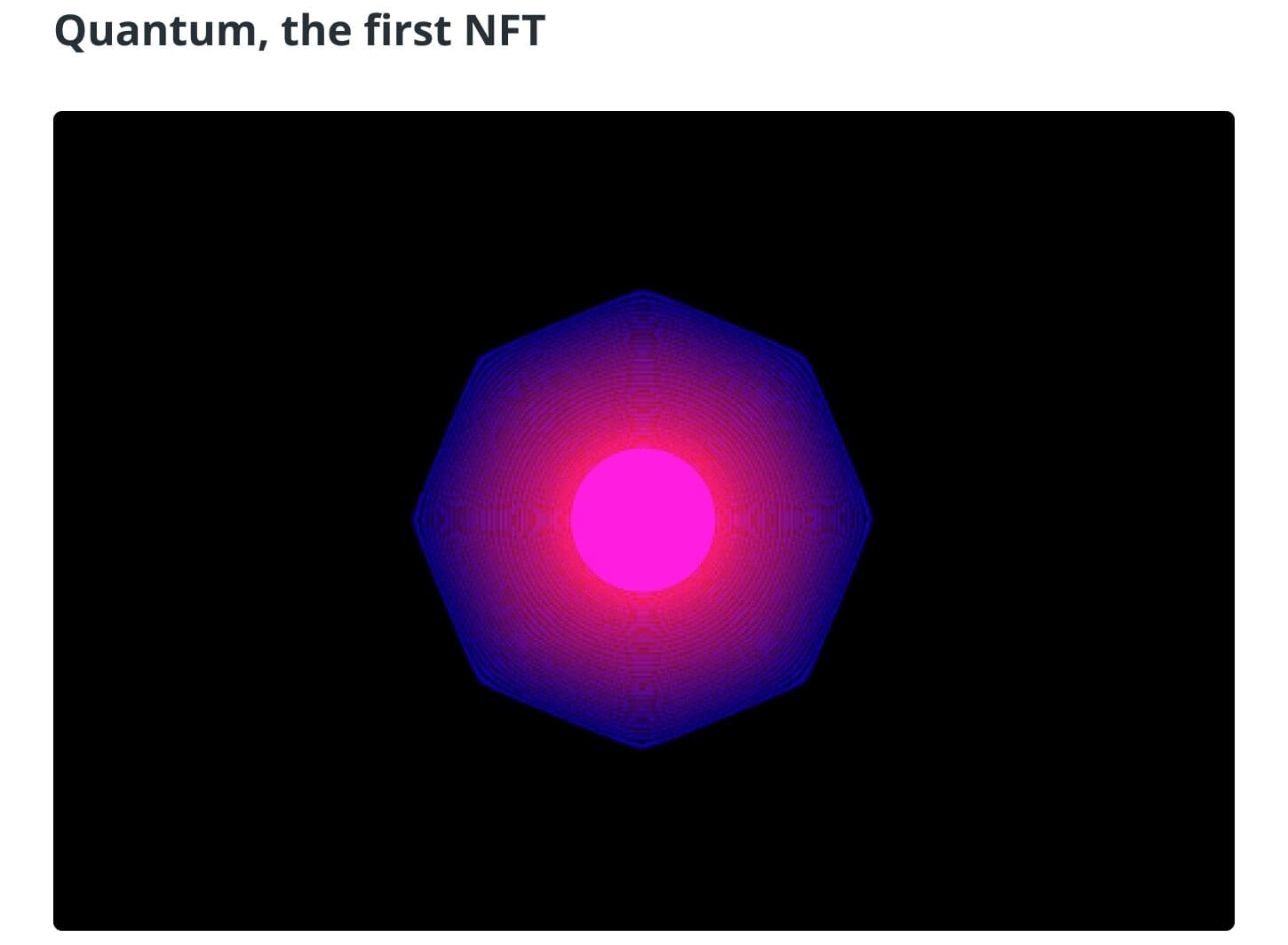

Despite the fact that 2021 ended up being the year of nonfungible tokens (NFTs), the technology wasn’t really created in that year. 2014 saw the creation of the first NFT, “Quantum,” by Kevin McCoy on the Namecoin blockchain. Nevertheless, the notion that resulted in the creation of BRC-20 tokens was first introduced with the introduction of Bitcoin-based coloured coins in 2012–2013. Meni Rosenfield first proposed this notion in a 2012 paper, which paved the door for the development of digital tokens on the Bitcoin blockchain.

NFTs, however, became well known in 2017. This was primarily brought about by the introduction of the Ethereum blockchain, which overcome the shortcomings of the blockchains that came before it in terms of hosting NFTs. Ethereum not only cut the barrier to entry for starting NFT companies but also gave NFTs a dependable solution for crucial issues including token creation, storage, programming, and trading.

NFTs Evolution: Coloured Coins To The Emergence Of Spells Of Genesis And Rare Pepes

As previously stated, coloured coins were developed to symbolize and manage ownership of real-world assets on the blockchain. These coins served as the starting point for the plot. Due to the “nonfungible” component that gave them a unique utility, they were distinct from Bitcoin (BTC).

Coloured coins represented a tremendous advance in Bitcoin’s capabilities because they were made of miniscule fractions of a Bitcoin, often as small as a satoshi. People began to understand the potential of blockchains for issuing assets thanks to use cases of coloured coins, such as the depiction of property, coupons, or usage as digital collectables, subscriptions, shares, and access tokens.

But coloured coins have only existed as a notion since Bitcoin was never meant to be used as a database for tokens. NFTs were ultimately created as a result of a series of research initiatives that were sparked by the development. As was previously mentioned, “Quantum,” an animation in the shape of an octagon, was the first NFT. The introduction of Ethereum gave NFTs the platform they needed to take off.

The Counterparty platform, which was based on Bitcoin, was a significant project of this period that made it possible for the development of digital assets. The use case for NFT as the artwork was launched when a range of “Rare Pepes” NFTs was made available on The Counterparty. Following “The Counterparty,” another significant NFT project was “Spells of Genesis,” created on Ethereum.

From CryptoPunks To Axie Infinity: The Rise Of NFTs In Gaming And The Metaverse

The continuous progress of NFTs toward the blockchain was made possible by Ethereum’s introduction of a set of token standards. Developers can deploy new tokens using information from the token standard.

Following the popularity of the Rare Pepes, software development company Larva Labs introduced CryptoPunks, its own generative series of NFTs developed by John Watkinson and Matt Hall. The creation, which was inspired by London punk culture, consists of 10,000 unique components, with no two characters looking alike. The Bored Ape Yacht Club, one of the largest NFT collections, and many other NFT ventures were built on the success of CryptoPunks.

The following significant launch was CryptoKitties, which took place in October 2017 during the ETHWaterloo hackathon. Players can purchase, sell, and construct NFTs in the game that represent idealized virtual cats on Ethereum. After CryptoKitties, NFT gaming grew in popularity.

NFT gaming and metaverse initiatives worked together to create new momentum. The Ethereum-based virtual environment Decentraland, which enables users to explore games, develop, and gather assets, was a significant initiative of this time period.

An NFT-based battle game called Axie Infinity was released in October 2018. Play-to-earn (P2E) games, which allowed players to earn in-game incentives while playing, were launched as a result. It’s a groundbreaking game on the Ethereum blockchain that features Axies, creatures that are uncommon NFTs with unique characteristics. Axies are used by gamers to combat fights while adding fresh characteristics to them.

Read more: Launching An NFT Collection? Avoid These Top 5 Mistakes For Success

Ethereum Expansion: Non-Ethereum Blockchains And The NFT Ecosystem

NFTs experienced a sharp increase in 2021 due to an array of factors. New standards were established by different blockchains specifically for NFTs.

In 2021, the supply and demand for NFTs both increased. NonFungible.com, a provider of NFT data, reports that over the year, NFT trading increased by about 21,000% to reach $17 billion.

One of the main causes of the increase was the use of NFTs in the art sector. The rise of digital art gave artists another platform to display their originality and store their work, which could also be independently evaluated. These benefits allowed digital art to grow rapidly and led to the NFT boom.

Famous auction houses like Christie’s and Sotheby’s moved their auctions online during this time. These auctions also featured artwork that contributed to the rise in popularity of NFTs. The record-breaking sale of $69 million for Beeple’s “Everyday: the First 5000 Days” NFT occurred at Christie’s. A transaction of that size caught the interest of blockchain aficionados and non-Ethereum blockchains.

As a result of the NFT craze, blockchains like Cardano, Solana, Flow, and Tezos began developing their own NFT platforms. Cardano introduced smart contracts in September 2021, enabling the creation of NFT apps on the network. Several new criteria have been established by different blockchains to verify the legitimacy of nonfungible assets.

The rebranding of Facebook as Meta and its entrance into the metaverse was a significant event of the year. NFTs have become increasingly popular since they have always been a crucial component of the metaverse.

NFT Market Recovery And Issuance Of NFTs With Bitcoin As Their Native Currency

The sector experienced a decline in 2022, but regained an upward trend in 2023, restoring NFT enthusiasts’ pleasure.

Growth in the NFT sector stalled for a large portion of 2022. The excitement in the NFT market was reduced by macroeconomic considerations. Even the metaverse had been a topic of discussion before it disappeared. In 2022, Mark Zuckerberg’s Metaverse subsidiary suffered a loss of $13.72 billion.

NFT fans, however, were once again grinning in 2023. Utilizing the 2021 Bitcoin Taproot upgrade, which allowed for on-chain NFTs to be native to Bitcoin, Ordinals began in January 2023. By February 2023, “TwelveFold,” a brand-new NFT collection to be issued on the Bitcoin network, has been officially announced by Yuga Labs, the world’s leading NFT issuer. Ordinals are a development of colourful coins that include serial numbers engraved on each individual satoshi.

Read More: The BRC20 Token Boom

The NFT market saw $2 billion in total trading volume in February, up 117% from the prior month, according to statistics from DappRadar. Data show that the momentum continued into March, with only a tiny decline to under $2 billion. By 2027, according to BCC Research, the NFT market will be worth $125.60 billion, growing at a compound annual growth rate of 27.7% from 2022 to 2027.

The overall number of NFTs sold in March was about 5.8 million, down from nearly 6.5 million in February, according to accumulated data from DappRadar and Dune. The amount of Ethereum NFT trading in February ($1.81 billion) and March ($1.82 billion) was nearly comparable.