The use of cryptocurrencies in the US and regulatory firms such as the SEC (Securities and Exchange Commission) are interested in finding out if the users are reporting their transactions for taxation. If any user fails to report their transactions to taxation, then they face the likelihood of being imposed fines and charges.

Let us find out how the cryptocurrencies are taxed in the US.

Cryptocurrencies are subject to tax in two ways. For the government to impose taxes on your crypto assets, you must have been involved in a buying or selling transaction. The cryptocurrencies are taxed in 2 ways:

1. Capital gains tax

This applies to profits that one makes after selling the asset at a higher price than the buying price. Profits must undergo taxation. Cryptocurrencies or assets that are held by the users for less than a year are considered short-term gains while the ones that are held for more than a year are referred to as long-term gains.

Buying goods and paying for services using cryptocurrencies subjects them to taxation just like fiat currencies. Instances such as buying NFTs using cryptocurrencies are also supposed to be taxed.

Trading your cryptocurrencies for fiat currencies also renders them subject to taxation.

2. Income tax

This tax is applied to cryptocurrency transactions that are made from mining and staking tokens. When a person is paid using cryptocurrencies after offering a service, this is considered a scenario where income tax applies.

Also Read: How Tax-Loss Harvesting Can Be Used To Reduce Losses

Long-term Crypto Tax Rates

These tax rates apply to assets that have been held for more than a year. Single individuals will not be taxed on amounts summing up to $44,625. Rates ranging from 0% to 20% apply to people who are married or the head of the household.

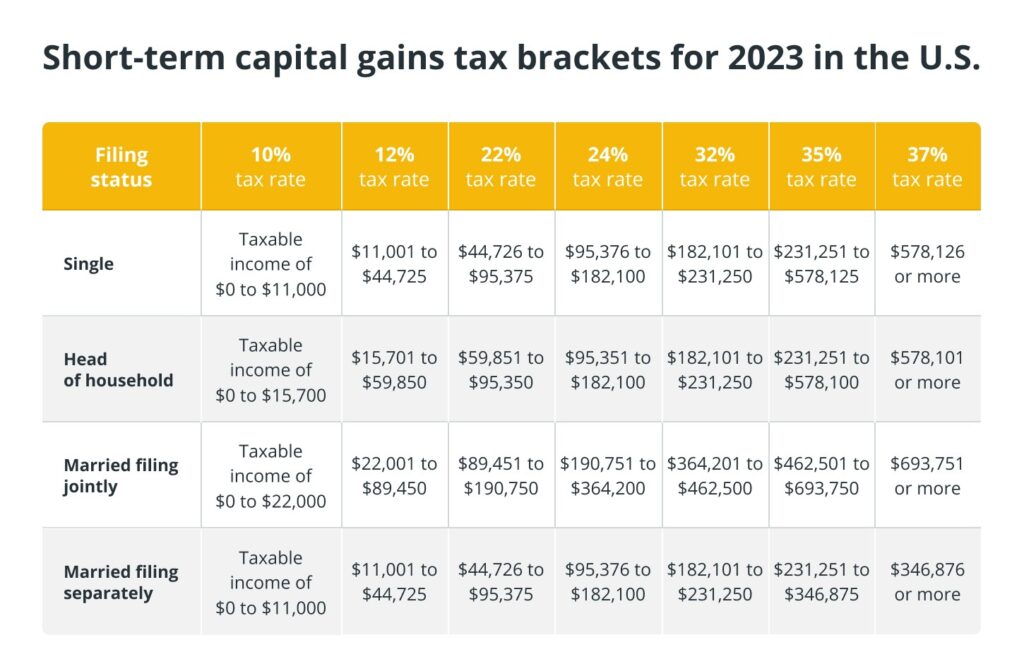

Short-Term Crypto Tax Rates

As mentioned before, short-term gains are assets held for less than a year. The taxes imposed on these currencies will be calculated regularly ranging from 10% to 37%.

Scenarios Where Cryptocurrency Transactions Are Not Taxed

- Using fiat to buy cryptocurrencies.

- Maintaining cryptocurrencies on your portfolio without selling them.

- Transferring your holdings from one wallet to another.

- Creating Non-Fungible-Tokens

- Making donations to charity using your assets.

- Giving gifts in the form of cryptocurrencies which are less than $15,000

Also Read: New Crypto Tax Laws In The US

Tracking Your Crypto Transactions

It is important to get hold of your data and check whether each one of them is supposed to be taxed or not. There are a variety of platforms that can help you do this by providing statements. Some of these platforms include Koinly and Accointing.

If you wish to do this on your own, you can follow these steps to achieve your objective:

- Take note of each transaction and organize them. Tabulate each entity. Some of them include the wallet addresses, the amount involved, and the time it happened.

- Integrate the cost basis for each transaction performed. Include the transaction costs and the purchase price fees.

- Calculate the losses and the gains made. To do this, get the difference between the cost basis and the fair market value of the asset during the time the transaction was being performed.

- Divide your transactions into two: the short-term and the long-term-based transactions.

Noting Down Crypto Holdings On Your Tax Report

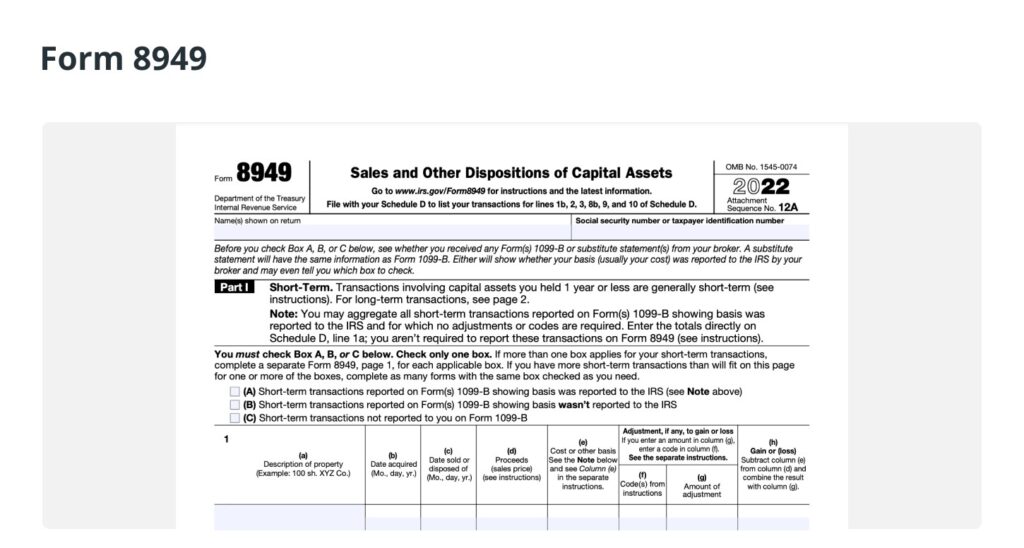

According to the Crypto Tax Form 8949, you are required to fill out the sales of crypto assets. In the form, there is a section where you fill out the short-term disposals and the long-term disposals.

It is important to indicate whether the transaction that you carried out was recorded on Form 1099. This is a form that is used by crypto exchanges to record income types throughout the year. These include stock investments and cryptocurrencies.

Section C on Form 8949 applies to short-term transactions that hadn’t been reported before. You have to give the following information when filling out the form:

- The type of asset sold.

- The date the asset was acquired

- The cost basis

- The fair market value

- The gain or loss

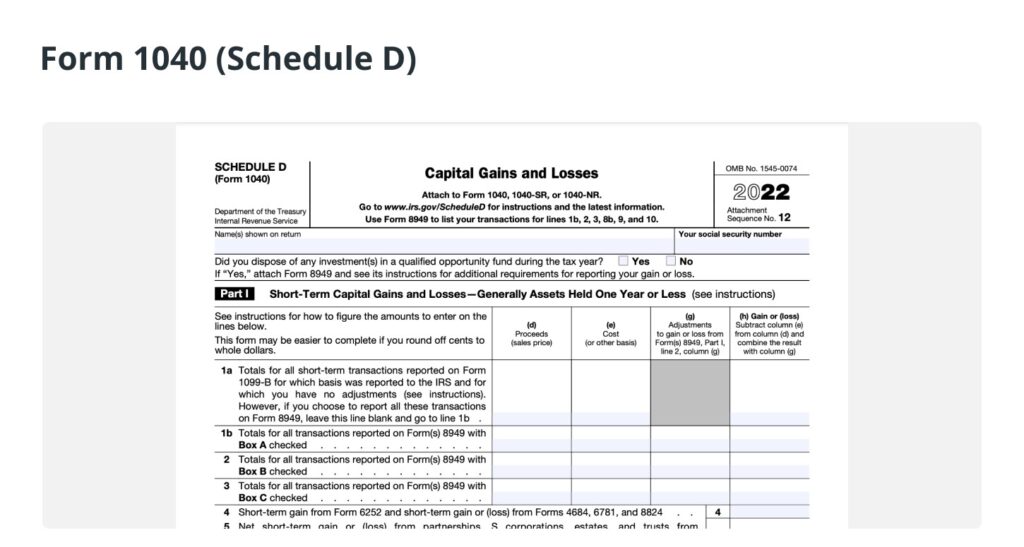

After filling out the form, you must transfer the gains or losses made to the Schedule D of Form 1040.

Making A Report On Your Crypto Income

This can be done on Form 1040 which is the commonly used form for individual taxes. All the gains and losses that have been made together with the total crypto income should be indicated on your form.

In the form, there is a section that asks whether one made money from crypto or received the crypto in the form of a reward or compensation. It also has a question asking whether someone sold or exchanged a gift in the form of a cryptocurrency.

All earnings made from buying and selling of goods and services must be made in the Schedule C section of the form. Crypto income made from airdrops, forks, and other sources such as wages and hobbies should be reported as other income on the form.

It is advisable to consult with the relevant authorities before filling out the forms to ensure you have captured everything correctly.